1. The History of Consortium System

We must take a step back to the 20th of March 1941, in order to reconstruct the legislative landscape that gave life to CONAI, the day in which the issue of material and waste collection in homes appeared in the national normative corpus and was declared an issue of public interest. A central office for solid municipal waste was born within the ministry of internal affairs. In truth, these facts are more useful from a historic rather than practical viewpoint, these measures were adopted during the Second World War and had very little effect on daily life. In order to delineate an actual involvement of the production system and citizens in the management of waste, we must wait until the DPR 915 from 1982, a consequence of the 1974 European directives, which introduced hygiene norms and the safeguard of health and the environment when disposing and managing of waste.

Six years later, Italy introduced a procedure on the reduction of waste and separate waste collection through law 475/1988, introducing an ecotax on plastic bags (100 Italian lire at the time) as well as requiring producers of plastic objects to collect and recycle this material, anticipating the philosophy of the European Directive from 1994. Even though law 475 was not able to give way to separate waste collection, it introduced some key elements for the future of the collection and recycling system, including the establishment of compulsory consortiums for specific materials (glass, plastic and metal). Replastic is one of the most important, it started operating in the nineties and will be the prototype for the future CONAI consortium system.

Italy has pioneered the introduction of compulsory consortiums for manufacturers and recyclers on a European level in 1997 with a great reform of this sector carried out by the Ronchi Decree (Dlgs 22/1997) that regulated the disposal and management of waste, promoting separate collection and recycling (before 1997, separate waste collection and recycling were not taken into consideration by the Italian industry, especially municipal waste, even though some types of waste, like iron and cardboard, had always been reused by businesses). The Ronchi Decree aligns Italian norms to the principle of “he who pollutes has to pay” and introduces the community principles of integrated waste management, shared responsibility and prioritises separate waste collection in waste management. The 22/1997 legislative decree implements the 04/62 directive on packaging waste, stating that packaging producers must fulfil their duties autonomously or through a collective system organised according to the model of private law consortiums (CONAI and other consortiums) that will carry out the collection ad recycling of packaging waste.

Nearly 10 years later, the 152/2006 decree finally established the waste cycle proposed by Dlgs 22/97, setting a new objective for public administrations: reaching 65% of separate waste collection by 2012. This objective has yet to be reached. The target for packaging waste was to reach 60% of recovery by 2008, this objective was reached very early. Specifically, at least 55% (up to 80%) of this 60% must come from recycling, assigning a more marginal role to energy recovery: this objective was also reached. Finally, through Dlgs 205/2010, Italy applied the objectives of the 98/2008 directive on the product fraction quotas of waste that must be recycled in addition to packaging waste.

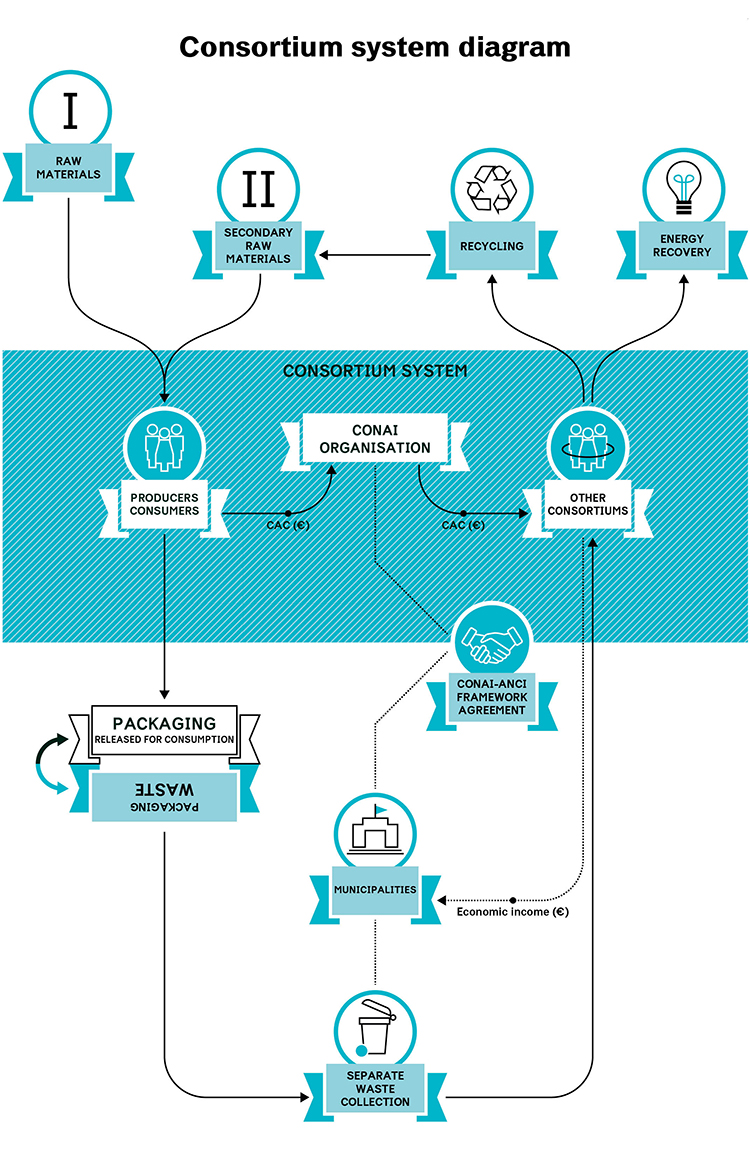

Dlgs 152/2006 tasks CONAI with ensuring the achievement of global recycling and packaging recovery objectives on the national territory, as well as the implementation of management policies, including those aimed at prevention through innovation.

Specifically, the Decree dictates that producers and consumers of packaging must form the Consortium, made up of private companies that participate in equal manner, whilst guaranteeing coordination with the separate waste collection activities carried out by public administration. Therefore, CONAI is a private law, non profit organisation, supported by a statute approved by public authorities with the aim of fulfilling the packaging waste recycling and recovery objectives established by the national law that applies European directives. In order to fulfil its duty, the Consortium (that has total managerial and organisational autonomy), coordinates and guides the activities carried out by the 6 packaging material Consortiums (CiAL, aluminium – COMIECO, paper and cardboard – COREPLA, plastic – CoReVe, glass – Ricrea, steel – RILEGNO, wood).

Consortium management in Italy follows a “unique model” in the waste management sector, since a matter of public interest is pursued by a private body: environmental protection, sharing the responsibility between companies, public administration and citizens from the production of packaging to its to the end of life stage. Even though the consortium system is not the only type of organisation that can handle packaging waste (if producers follow specific conditions they can organise autonomously or give birth to an alternative restitution system), CONAI was the centre of the managerial model chosen by Italy in order to reach the recovery and recycle objectives determined by European directives since its inception. If a producer who decides to independently manage the recovery of its packaging does not reach the appointed targets, it will be forced to join the consortium.

Specifically, CONAI’s functions are defined in article 224 of Dlgs 15/2006; this is a summary of said functions:

- define the environmental areas where to instate an integrated collection, selection and transport system for materials selected at collection centres, in collaboration with regions and public administrations;

- define the general conditions for the withdrawal of waste coming from separate waste collection;

- elaborate and update the General Program for the Prevention and management of packaging and packaging waste (PGP) and the Specific Prevention and management plan for packaging and packaging waste (PSP);

- promote program agreements with economic operators in order to support recycling and recovery of packaging waste and ensure it is carried out;

- ensure the cooperation between the consortiums and other economic operators, in order to achieve the global target set by the legislator in 2008, which states that at least 60% of the weight of packaging waste compared to what was released for consumption and the recycling of at least 55% (up to 80%) of the weight of waste compared to what was released for consumption must be recovered. In order to reach these objectives, CONAI sometimes operates by sending a quota of the environmental contribution to the consortiums that achieve higher quotas of recovery and recycling that what is indicated by the General Program;

- guide and ensure the connection between public administrations, consortiums and other economic operators;

- organise information campaigns deemed useful for the implementation of the General Programme, in agreement with public administrations;

- determine the CONAI Environmental Contribution (CAC) that each consortium member must provide, through the modalities selected by the Statute;

- promote the coordination with the management of other types of waste;

- promote agreements between consortiums/consortium members and public/private entities on a voluntary basis;

- provide data and information requested by Authorities;

- acquire the data relevant to incoming and outgoing packaging flows on the national territory and data regarding other economic operators from public or private bodies involved in the process.

Furthermore, CONAI is able to stipulate a national framework programme agreement with the ANCI (Associazione Nazionale dei Comuni Italiani, National Association of Italian Municipalities), with the UPI (Unione Province Italiane, Union of Italian Provinces) or with relevant authorities, in order to guarantee the accomplishment of the principle of managerial co-responsibility between producers, users and public administrations.

1.1 Consortium members and the CONAI Environmental Contribution

When producers and consumers of packaging join CONAI and, only in the case of producers one of the six Consortiums, they must pay the CONAI Environmental Contribution (CAC), which is determined by the BOD on a yearly basis and differentiated according to the type of packaging. The CAC is the main source of the funds that are redistributed between producers and consumers according to the costs of separate waste collection, as well as the costs of recovering and recycling packaging. The Environmental Contribution applied at the time of the “first cession” (i.e when any type of permanent or temporary transfer of complete packaging from the “final producer” to the “first consumer” takes place on the national territory or packaging material created by a “producer of raw material or semi-finished products” for a “self-producer”) is managed by CONAI, that represents the other consortiums and their interests. CONAI withholds a quota for the completion of institutional activities, and distributes the remaining part to the six Consortiums that are tasked with organising the collection of paper, glass, plastic, wood and metal (steel and aluminium) packaging waste separately collected within municipalities, as well as the processing and delivery to the final recycler, that could be a single facility or a certified intermediary. The consortiums, must then proceed to pay Municipalities according to the quantity and quality of collected packaging.

CONAI is the largest Italian packaging and packaging waste management consortium, with more than 850,000 consortium members; 99% of consortium members are packaging users, mostly made up of business operators (more than 480,000 entities) and “Other Users” (more than 300,000 entities) followed by food companies (51,000) and the chemical sector (nearly 3,000). Only 1% of consortium members are packaging producers, mostly represented by the paper, plastic and wood packaging sectors.

1.2 Economic flows of the consortium system

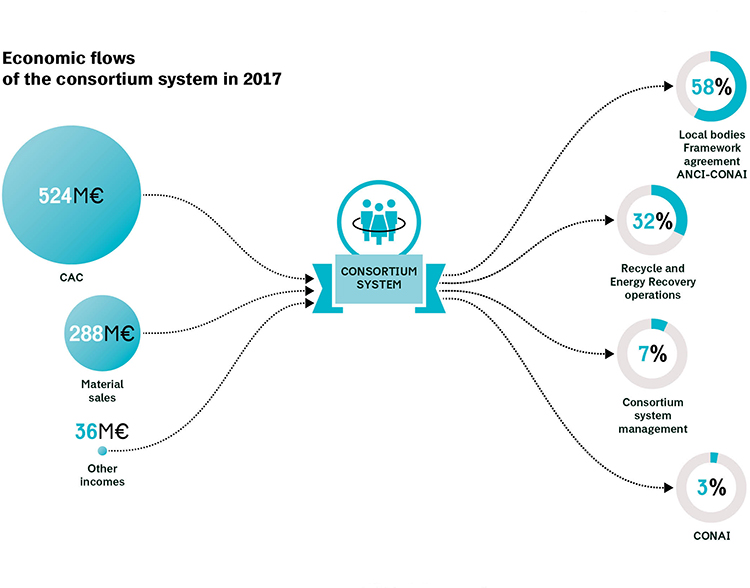

The Consortium’s overall economic flow for 2017 resulted in approximately 849 million euros of income, mainly deriving from the CONAI Environmental Contribution (CAC) which provided 524 million euros, in addition to the 288 million euros coming from material sales and 36 million euros from non characteristic, financial and extraordinary management.

Management costs were equal to 875 million euros in the course of the same year, 86% of which came from conferral, collection and recycling costs (logistics, selection, pre-treatment, etc.):

58% of these costs came from the sums given to public administrations in the context of the CONAI-ANCI framework agreement, in order to cover the costs of separate packaging collection and packaging waste (conferral);

32% is destined to consortiums, as a remuneration for companies in charge of the withdrawal and recovery of collected material;

10% was used to cover the costs of the consortium’s structures, as well as other costs for specific activities throughout the national territory, ordinary and extraordinary territorial projects, educational and communication campaigns aimed at citizens and so on, a further advantage for local authorities.

The negative balance between incomes and costs was absorbed by consortiums: each one gave their quota, using the savings generated by the economic surplus accumulated in recent years.

1.3 The Framework Agreement and the relationship with municipalities

The ANCI-CONAI framework agreement is the instrument used by CONAI and Consortiums to ensure that approved Municipalities are able to withdraw packaging waste collected separately and receive the correct economic compensation, relative to the higher costs of separate waste collection. The agreement between CONAI and ANCI is voluntary, as stated by article 224 of the 152/2006 Dlgs, and operates as a subsidiary to the market, and includes the possibility for municipalities to subscribe to an agreement that tasks them with collecting packaging waste separately and confer the material to the consortiums. On the other hand, Consortiums guarantee the withdrawal of said material, its recycling and an economic remuneration equal to the quality and the quantity of conferred material.

The agreement is made up of a general section, where the principles and shared application modalities are illustrated, and six Technical Attachments (one for each material) that discipline the contents of the agreements with each municipality, which can be signed directly or through another delegate.

The first Framework agreement between ANCI and CONAI was signed in July of 1999 and was valid until 2003; this agreement helped kick-start separate waste collection aimed at recovery. The agreement was made up of five technical attachments for paper, plastic, wood, steel and aluminium, whilst the management of glass packaging was disciplined by the Ministerial Decree of the 4th of August 1999. The main principles of the agreement, that have been strongly confirmed in future updates were:

- Guaranteed volumes: Consortiums were tasked with collecting packaging waste even beyond the limits set by law. Furthermore, municipalities were able to confer similar fractions, processed recycling agencies, directly to the system;

- Guaranteed value: Increased costs for the collection of packaging were covered, in accordance with the quantity and quality of gathered material, in order to ensure maximum efficiency;

- Guaranteed time: the agreement lasted five years, in order to give interested parties (Municipalities and managing bodies) the time to plan medium term management systems for municipal waste, as well as the time to tackle long term investments;

- Guaranteed transparency: through the coordination and monitoring of committees set up by ANCI and CONAI – Consortiums connected to territorial projects;

- Guaranteed subsidies: compared to the market value of packaging waste conferred through separate waste collection;

- Guaranteed roles: respecting reciprocal autonomies of ANCI, CONAI and Consortiums;

- Guaranteed quality: i.e. the purity of collected materials, since the theme of quality was very important since the first iteration of this agreement, due to the fact that recycling must be guaranteed through sustainable economic and environmental conditions;

- Growth of collection levels in struggling areas: this was also pushed by supporting the improvement and homogenisation of separate packaging waste collection levels on a national scale.

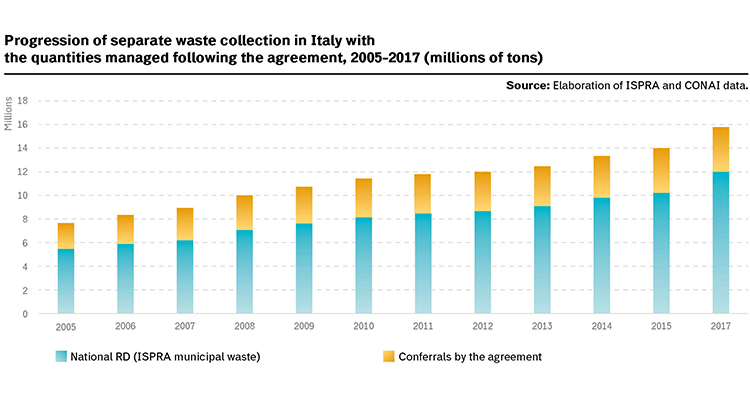

In those years, separate municipal waste collection was still marginal: in 1999, only 4 out of the 28 million tons of municipal waste were collected separately, the rest was sent to landfills. After the first agreement expired, separate waste collection rose from 13% to 21%, with 6 million tons collected out of a 30-million-ton urban waste production: the use of landfills dropped by 60% (5 million tons less waste). The agreement was effective and useful to push local bodies to create new separate packaging waste collection systems, since they could count on the guarantees provided by the agreement; this generated a sort of domino effect on other types of municipal waste. The quantities conferred to Consortiums thanks to the agreements stipulated throughout the national territory in 2003 reached a total of 1.6 million tons, 26% of the total waste gathered.

ANCI and CONAI signed the second Framework Agreement in December of 2004, which expired in December of 2008. The objective (shared by the six Consortiums), was to confirm the guarantees given in the first Agreement, whilst introducing mechanisms aimed at supporting further qualitative and quantitative improvements for waste collection. The agreement was structured in a similar manner, but some general innovations were adopted, including the themes of prevention in respect of the European hierarchy, with a strong focus on the quality of conferred material, the use of recycled material for production and increasing green purchases, especially for public administration.

The push towards a constant growth of separate waste collection was effective, so much so that by the end of 2008, the amount waste collected separately on a national level reached 31% (10 million tons) and disposal rates dropped by 49%: Consortiums were given 2,9 million tons, a 47% increase from 2004.

The third Framework agreement was valid from 2009 to 2013, and it maintained the same basic structure. Furthermore, even though it had already reached the recovery objectives set by the 2008 legislation within a market that was not favourable to raw and secondary material (which dropped by 40% compared to the prior year), the system continued to collect packaging waste on the whole national territory, paying the largest part of the costs of separate waste collection. This agreement included a yearly increment of fees by 2/3 of the inflation rate, as well as increasing the efforts towards improving the quality of separate waste collection in order to enhance efficiency and reduce the amount of waste sent to landfills. Other important innovations were:

- technical attachment for glass packaging: COREVE (the Consortium of Glass Recovery) singed the technical attachment for the withdrawal of glass packaging for the first time, giving municipalities a chance to subscribe to the conventions of all packaging industries.

- supporting struggling areas: all parties decided to support the growth of collection in struggling areas with a greater use of resources and instruments, in order to help the regions with the lowest packaging waste collection rates.

- efforts towards training and communication: a timetabled and systematic training activity aimed at local administrators from struggling areas was instated, as well as the support to local communication campaigns for the development of collection and recycling of materials separated by citizens.

- market subsidiarity: the subsidiary role of the system was confirmed by the ability of Municipalities and authorised operators to move within the agreement. Consortium members were able to give up their conferral obligations within specific time frames, sending their material on the free market. The convention’s framework could be re-joined within predefined time periods.

Separate waste collection on a national level reached 12 million tons by the end of 2013, equal to 42% of municipal waste production, whilst disposal dropped to 37% (11 million tons). By the end of 2013, the amount of packaging conferred by consortium members was 3.4 million tons, a 7% increase compared to 2009.

The fourth Framework Agreement was signed in April of 2014, and is still active today; it regulates the relationship between authorised Municipalities and consortiums for the five-year period between 2014 and 2019. This new edition of the Agreement still maintains the same structure used in its previous iterations, confirming the guiding principles and the fundamental characteristics, including subsidiarity. This characteristic was reinforced in the new Agreement, since members can now adhere to or recede the agreement with no break in continuity, as long as they respect an appropriate notification period. Thus, Municipalities can decide to give up their conferral obligations and manage the recycling of gathered material themselves. They can also abandon the agreement and re-enter it within predetermined time frames. In addition, the support to integrated management systems was strengthened in areas of the countries that are struggling to keep up with the performance standards dictated by law.

Collaboration with municipalities spurred the growth of separate municipal waste collection since the guarantee of packaging recovery (approximately 25% of the total) promoted the separation and exploitation of other product fractions, especially organic, with significant positive effects on the environment and economy. According to the latest ISPRA update, separate collection reached 52,5% in 2016, and disposal at landfills was at 29%. During the first three years of this new agreement, conferrals dictated by the agreement grew from 3.5 to 4.1 million tons (a 16% increase). Nevertheless, it is still useful to report that some fractions included in the calculations of separate waste collection from the new method adopted by ISPRA in the course of the last year, reported by Dm of the 26th of ay 2016 (especially scraps from multi-material waste collection, construction and demolition waste, sweeping soils and sands), cannot contribute to the recycling objectives provided by directive 2008/98/CE. Therefore, this determines an increase in the margin between percentage of separate waste collection and recycling of municipal waste.

The quota of packaging waste collected by following the agreement grew from 2.2 million tons to just above 4 million tons between 2005 and 2017, nearly 42% was glass, 25% paper, 26% plastic packaging, 3.6% steel, 3% wood and finally 0.4% aluminium packaging. During the same time period, all materials (except wood that decreased by 3%) showed significant increases: plastic and aluminium conferrals trebled, going respectively from 360,000 tons to more than 1 million and from 5,000 tons to 14,000 tons; the numbers for glass doubled and reached 1.7 million tons of packaging conferred in 2017 compared to the 652,000 tons from 2005; improvements for steel and paper were modest but still relevant, respectively 3% and 10%.

Conventions

The number of municipalities served increased progressively in the course of the years, showing good presence on the whole national territory. Aluminium and wood increased the number of agreements respectively by 23% and 20% between 2005 and 2017, serving approximately 13 million more inhabitants. The plastic industry returned to the figures it had reached in 2005, with an 85% coverage of served municipalities; this number oscillated between 90% and 91% between 2008 and 2015. The paper industry has decreased its coverage by 6%. This reduction was caused by the choice of Municipalities to process gathered materials on their own, but we must underline that recycling activities are still very high. The Glass Recovery Consortium (that entered the Agreement in 2009), has increased its territorial coverage by 17%, serving 9 million more inhabitants. On the whole, the number of people covered through the 2017 agreement goes from 68% for aluminium and wood to 93% for plastic, 92% for glass, 84% for paper and 82% for steel.

Fees

Consortiums provide members with an economic fee for the costs of separate packaging and packaging waste collection that must be carried out according to the principles of efficiency, effectiveness, cost-effectiveness and transparency.

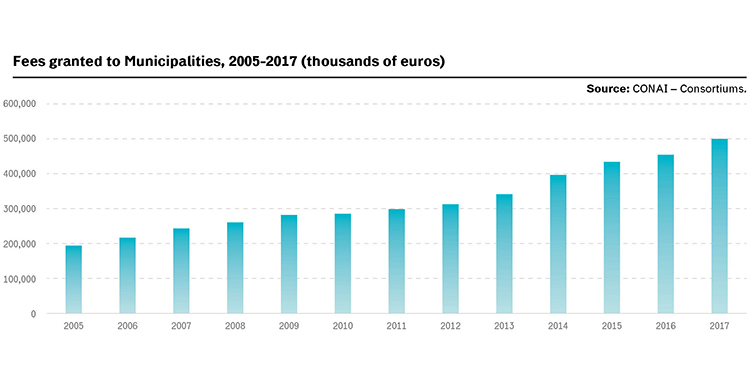

The fees given to Municipalities have grown substantially, going from 195 million euros in 2005 to 500 million euros in 2017.

On the whole, the system has granted municipalities more than 4.2 billion euros between 2005 and 2017.

Public administrations on the whole national territory can rely on the Framework Agreement that guarantees universal withdrawal, meaning that withdrawal always takes place with no quantitative limits, even when environmental objectives have already been reached and surpassed, but with well defined qualitative conditions, sustaining the costs of selection and processing, and withdrawing all types of waste, even those of lower quality.

1.4 A survey on circular economy to improve CONAI efforts towards prevention

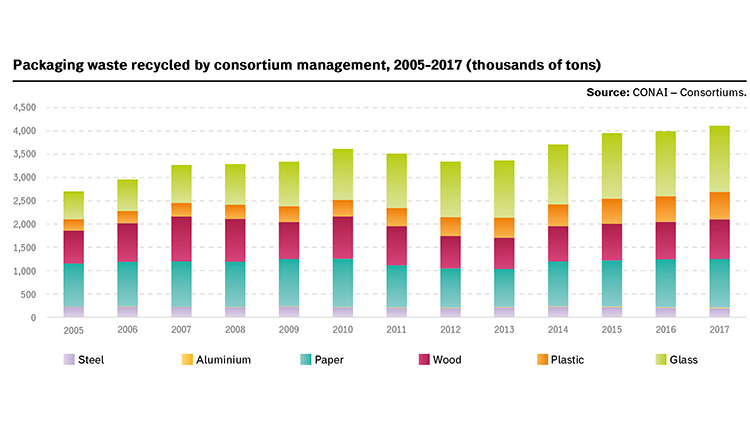

The amount of waste recycled by the consortium system has surpassed 4 million tons in 2017 and has constantly increased in the last few years (50% more than 2005). Italy recycles 47% of packaging waste, and the remaining part is handled by independent operators.

Glass is the main component that determines the weight of waste recycled in 2017, with a quota of approximately 35% (1.4 million tons); the next in line is paper packaging waste with a little more than 1 million tons, and wood with 850,000 tons, that respectively represent 25% and 21% of the total; plastic provides 587,000 tons, steel 193,000 and finally aluminium, with 14,000 tons.

Percentages have varied slightly in the time period considered by the analysis: in fact, paper and cardboard waste were the waste types that contributed most to the weight of recycled material with a 34% quota, followed by wood and glass, respectively representing 26% and 22% of the weight.

The steel industry registers a 13% overall decrease in recycled material between 2005 and 2017. On the other hand, the numbers for aluminium have quadrupled between 2005 and 2017, showing a prevalently growing trend in the last few years. Glass and plastic have also doubled the quantity of recycled waste in the analysed period. Wood and paper have respectively increased by 20% and 13% in the course of the same time period.

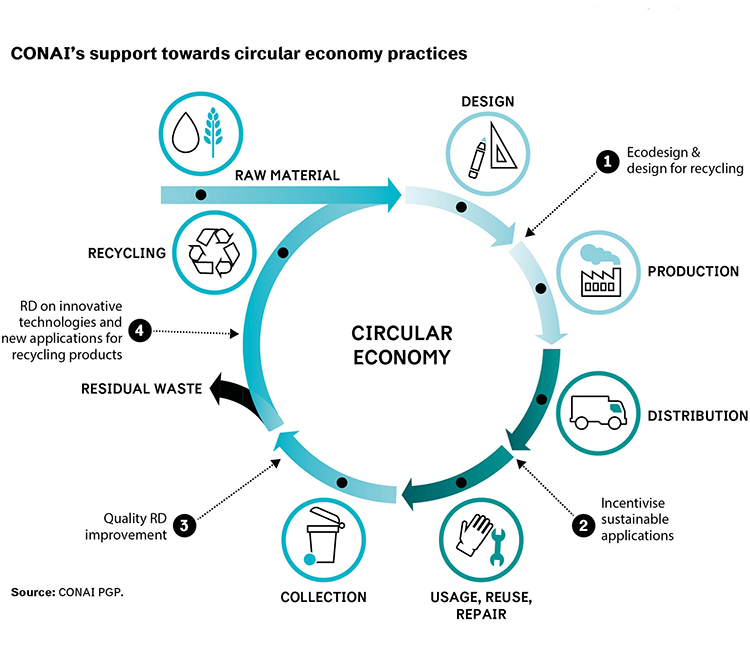

According to Dlgs 152/2006, CONAI must support companies in the promotion of actions aimed at reducing the environmental impact of packaging waste and improving the management of said materials at their end of life stage. Every year, CONAI must elaborate a General Prevention Program that describes current and future initiatives (relative to the five years after publication), in order to affect every section of the industry, pushing it towards a more circular system that is increasingly more concrete and measurable.

These measures can be structural, i.e. bound to the exploitation of the leverage given by contributions as a form of prevention, and the role given to CONAI by legislators (for example the Framework Agreement for a high quality separate waste collection); these measures can also concern raising awareness and incentivising consortium members, under the umbrella of the “Pensare Futuro” (Future Thinking) project (the E-PACK online service, the Designing recycling web platform, the Eco Tool etc.).

In 2016, CONAI carried out a study named Circular Economy Scenarios: CONAI’s role, in collaboration with the Management Institute of the Sant’Anna School of Pisa and the Green Economy Observatory (GEO) of the Bocconi IEFE. The companies that adhered to CONAI and other consortiums with an annual turnover higher than one million euros and with more than 10 employees, were invited to answer an anonymous online questionnaire, aimed at investigating the levels of adhesion to the principles of circular economy.

The questionnaire addressed the four main categories of companies that are part of the consortium, i.e.:

- Packaging producers: “suppliers of packaging materials, manufacturers, transformers and importers of empty packaging and packaging materials”;

- Producers of secondary raw materials: “producers of material recovered after its previous use”;

- Industrial users of packaging: “users of packaging and importers of full packaging”;

- Traders and distributors: “traders, distributors and those in charge of filling packaging”.

The questionnaire helped understand the actions carried out by companies that produce and use packaging within the CONAI system, as well as the instruments they adopt in the various phases of the process, from the procurement of raw material, to product design, manufacturing and distribution.

Procurement, since the first step towards circularity implies we must rethink the raw materials used in the manufacturing process, and make the logistic entry phase more efficient.

Design, because packaging eco-design choices can take functionality and environmental impacts into account at the same time and in an integrated manner, for example by increasing the chance of recovery at a product’s end of life stage, or to extend the life span, or even by representing efficient reduction solutions in the use of raw material and/or facilitation for re-entry in production processes.

Production, due to the fact that making the manufacturing process more efficient and the implementation of new technologies are fields that have pushed the efforts of Italian companies towards more circular processes.

Distribution, because the way in which consumers use a product in addition to a correct management of its end of life stage are a key moment to kick-start the re-entry of materials into the production cycle. The sustainability needs of increasingly more aware consumers represent a strong influencing element on companies, not just in the choice of purchase: companies attempt to minimise the impact of their packaging at its end of life stage also by virtue of the consumers’ virtuous behaviour; consumers must then deposit waste in the dedicated containers.

Consumption because the way in which consumers use a product, combined with a correct management of the end of life stage of the product, represent a key step to re-insert materials in production cycles. The consumers’ sustainability needs (who have become more and more aware) exact a strong influence on companies when they are choosing what to buy, but it also pushes a company to minimise the impact of packaging at its end of life stage due to the virtuous behaviours of consumers, who deposit waste in the correct waste container.

40% of producers put packaging made entirely of recyclable material on the market. The main actions are represented by audits along the whole supply chain, aimed at identifying areas that need improvement (approximately 15% of producers has implemented or is implementing this procedure) and from the stipulation of strategic agreement with suppliers, with the objective of increasing the use of second quality raw materials (nearly 15% of producers has implemented or is implementing this procedure).

Packaging manufacturers are forced to pay attention to prevention, as stated in the 2016 Prevention Dossier Shared Future. Innovation, beauty and sustainability, we must strive to obtain the best performance with the lowest possible impact. Packaging covers multiple functions in a competitive globalised and fast market like the one that exists today: it protects and conserves, informs, avoids waste, communicates by identifying the product and entices the customer influencing his or her choice; design must respect these functions, or even better, improve them. Ecodesign must consider all the functions and prioritise the minimisation of environmental impacts throughout the products’ useful life cycle.

The indicators used to investigate the presence of Ecodesign are represented by the percentage of packaging designed with homogenous matrices (in order to facilitate recovery) and the average reduction of the weight of the packaging (expressed in percentages); more than 70% of companies designs packaging that contains homogenous material and approximately 60% designs them reducing their weight, therefore reducing the use of resources. Approximately 35% of companies decided to carry out initiatives aimed at improving logistics (for example by minimising empty spaces in the packaged product) in order to improve their circularity. Slightly more than 20% carried out initiatives to enhance the product’s disassembly process, which is undoubtedly a stimulating idea for future designers.

With regards to secondary raw material producers, approximately 50% choose matter containing only recycled material and nearly 60% uses packaging made exclusively from recycled material. 25% of the entities that were interviewed carries out the test for the total or partial substitution of raw materials with recycled raw materials.

The same key indicators used with secondary raw material producers relative to raw material procurement, semi-finished products and packaging, investigating the use of total or partial recycled material, were used in order to understand the actions carried out by industrial users in the procurement phase. The situation that emerges from this investigation has great room for improvement, that can take place by acting on the secondary raw material market and on the access to innovative technological solutions, where a little less than 40% uses raw materials and semi-finished products made with recycled material, but more than 40% already uses packaging made entirely with recycled material.

Strategic agreements with raw material suppliers aimed at creating collaborative and long lasting partnerships with the objective of broadening the use of recycled material in production processes are rapidly increasing.

Efforts in the fields of Research & Development represent a determining factor for the growth of the sector as a means to enlarge the market and improve competitiveness: studies aimed at finding solutions to minimise the environmental impact of a company’s product through an active involvement of suppliers (for example the collection of useful data and identification of areas that could improve) represent the most adopted second action.

Ecodesign in industrial applications (that mostly involves actions aimed at secondary and tertiary packaging), can ignore aesthetics to the advantage of functionality, whilst primary packaging “speaks” directly to the consumers and must therefore convince them to buy the product. The action carried out by more than 60% of companies is the development of finished products that can be recycled at their end of life stage, whilst more than 50% already puts products that can be disassembled into monomaterial components on the market, followed by products reused for different purposes and the actions aimed at reducing the amount of raw material used for the manufacturing of the finished products through alterations of their production cycle.

This research has also analysed the consumption of finished products, a phase that covers a vital role on the issue of prevention. The most interesting results show that more than 50% of the users gives correct information on where to deposit products after they have been used and approximately 40% provides information on the end of life stage management of packaging.

One more action we must bring to your attention is represented by the new ways in which the relationship with clients and customers is managed, for example direct supply (sometimes at the time of the first purchase, with the finished product) of substitutable components that can prolong the life of a product, as well as repair services even after the warranty has expired.

The role of a commercial distributor, both from the so called Great Distribution and the retail sector, is also very sensitive since its predisposition to circularity may have an impact on the transition phase from the current consumption model towards a sustainability that is more and more present in our daily habits. The retailer can decide to become a promoter for manufacturers of secondary raw materials and packaging, by putting goods with specific green characteristics on the market; he can be a spokesperson and orient the choices of his customers, connecting his image to the efforts towards environmental protection.

Today, 40% of distributors select products that are completely made out of recycled material.

To conclude, the questionnaire shows that the packaging sector could play a central role in the future of circular economy, in every phase, from production to the product’s final use.

Specifically, we must follow and support the consolidation of green procurement, facilitating access to secondary raw material, or matter made with high quality recycled material; we must incentivise a green approach in the manufacturing and packaging use sectors in order to generate a trickle down effect on the whole industry – it must be designed as a resource from its inception to the management of its end of life stage, as shown by the fact that one out of two packaging producers uses totally recycled raw material. Competent institutions and CONAI-Consortium system, must ensure that companies may adopt a long term circular strategy and be able to rely on a solid secondary raw material market, especially in terms of competitive prices and quality.

A considerable and increasing number of Italian companies have adopted the principles of Ecodesign, putting disassemblable products made with monomaterials and/or recyclable components on the market. This is even more evident in the packaging sector: in the last 3 years, nearly 2 of every 3 companies have worked towards reducing the amount of raw material used for a single packaging whilst maintaining its functions. What may seem obvious in the eyes of a consumer (like reducing the weight of packaging by one gram), requires research and technologies that can be adopted starting form the design phase. Companies that committed to researching and developing ecoinnovation and ecodesign solutions must be supported through the creation of new skills and know how, that can be easily accessed economically and bureaucratically speaking, in addition to whatever else may be deemed necessary.

1.5 The reuse observatory

The CONAI-Sant’Anna research has underlined the fact that more than 60% of industrial consumers reuses packaging for the distribution of the finished product. Reuse is a widespread practice that is also hard to monitor and quantify, since it is an integral part of the “good management” of Italian companies.

The Politecnico di Milano has been supervising the Reuse Observatory on behalf of CONAI since 2015, with the objective of mapping packaging reuse practices connected in Italy, taking the types of packaging, the sectors in which they are used, the diffusion of the phenomenon and the market size into account.

The types of packaging that were analysed are:

- steel regenerated kegs (chemical and petrochemical sector), truncated cone-shaped for foodstuffs, cages and pallets from regenerated multi-material cisterns, beer and olive oil kegs, pallets, canisters and various types of containers;

- aluminium CO2 canisters, other types of canisters, pallets, containers for chemical products;

- cardboard octabin boxes used for B2B experiences and in the same shop chain;

- wooden pallets, retention units, foldable boxes, reels, cages, crankcases and platforms;

- plastic regenerated kegs, jars and pallets for regenerated multi-material cisterns, collapsible boxes for food, layers, detergent bottles, cases and baskets for VAR transport, bowls used in water distribution, pallets, retention units, cases, octabins, bins and durable bags;

- glass water, soft drink and beer bottles.

The sector, main qualitative characteristics (size or average weight), any possible regeneration processes and the existing circuit have been identified for the packaging types we listed above. Some quantitative characteristics were identified where possible, for example the number of new packaging release for consumption versus regenerated packaging, annual movements, average number of reuses in the course of one year, average useful life and average substitution rate.

The observatory also presents LCA analyses for specific types of reusable packaging, aimed at evaluating the environmental impacts connected to the life cycle of multi-material cisterns, steel kegs for chemical and petrochemical products and reusable collapsible plastic boxes. The systems included in life cycle evaluations regard production, regeneration at the end of life stage of analysed packaging, whilst impact categories refer to the European Commission’s 2013 PEF Guide.

In general, all studies show that regeneration and reuse are environmentally preferable to single use products, and the advantages of reuse increase with every use of the same packaging in these specific applications. The main impacts connected to the regeneration phase are mostly bound to transport.

STEEL

Kegs, cages, canisters, pallets and industrial cases

The main sectors using these items are paint, food and liquefied and compressed gasses. The analysis shows information on the reuse of regenerated kegs (object of the CONAI memorandum from the 19th of March 2014), steel cages that protect plastic kegs in multi-material cisterns and gas canisters, monitored by the respective category associations.

With regards to food kegs, typically used to contain tomato pulp or fruit pulp, the estimated production for 2017 is estimated at 60% for truncated cone-shaped kegs.

Then there are kegs used for beer, their life span is 15 years, during which they are used 3-4 times in the course of each year.

Steel pallets can be found when hygiene or fire risks are present.

ALUMINIUM

Canisters and Pallets

Aluminium canisters are used for dietary gases or portable breathing apparatus. Aluminium pallets are used in the pharmaceutical, chemical and food sectors, in white rooms and all hygienic-sensitive sectors.

PAPER

The only experience so far comes in the form of octabins (prism shaped packaging with an octagonal base used to transport piece products, granulates or powders).

They are generally reused when the product they are carrying is light (small PET preforms for example). The number of reuses varies from 2 to 10 and mostly depends on the mode of transportation.

The CONAI Prevention Notice enabled to record reuse experiences connected o cardboard boxes used to optimise incoming and outgoing flows in factories, i.e. for the redistribution of goods towards various sales outlets on the national territory and cases of display units within organised large distribution.

WOOD

Pallets, industrial cases, retention units and coils

These types of packaging are used in various sectors. The data available on the reuse of pallets refer to procedures that entail benefits and simplification in the application of the CONAI Environmental Contribution.

Industrial cases can be separated according to specific types and their final use: foldable cases are the most reused type of case.

The reuse of retention units spans across various fields, from heavy industry to wine production and food.

The wood industry has always been active on the theme of reuse, especially for what concerns pallets.

“Bins” are typical pallets used to transport fruit. These products play a crucial role in the operational management of modern distribution, especially for consumer goods. Therefore, the supply chain is deeply important if we consider the fact that it is multiuse and multi-user and as such, its logistics, supply and return must be planned carefully.

Users from specific sectors rent pallets. The renter supplies the number of pallets needed by the user, who must then send products to its clients and communicates the location of the pallets to the renter, who will then withdraw them and use them once again. Rental companies manage the pallets used by their clients (manufacturers, distributors or logistics operators), creating their own withdrawal, control, selection and repair circuits as well as offering a rental service for all types of equipment.

This practice is not yet very present in Italy; it represents approximately 18%.

PLASTIC

Kegs and cisterns, boxes and baskets, pallets, industrial cases, water distribution bottles for offices and public places, layers used to transport glass bottles, flacons used for detergents and reusable durable bags.

The main reuse of plastic packaging is connected to fruit and vegetable baskets, where rental is an interesting sector: most pooling societies are part of the EURepack Consortium. The average life span of a basket goes from 5 to 20 years, and it undergoes an average of 6-7 annual rotations.

Other applications are represented by cases/baskets used to transport returnable glass bottles, that can be used up to 30 times.

Plastic pallets are often used in the food sector and are sometimes rented.

Industrial cases are prevalently used in the automotive and house appliance sectors: quantitative data on their reuse is critical, since this type of packaging is used in various industrial sectors, and prevalently in the realm of internal logistics.

Polypropylene layers (separation panels) make up 80% of the layer sector; their average life span (7 years) can vary according to the type of bottles it transports.

Water canisters used in dispensers can be made out of Polyethylene Terephthalate (PET) or polycarbonate (PC): currently, most Italian companies are using PET bottles, due to the presence of bisphenol in PC; this substance could disturb the endocrine system.

GLASS

Bottles

The circuit of “returnable” glass packaging includes the water, beer and beverage sector, and refers to distributors that supply Ho.Re.Ca (Hotellerie Restaurant Cafè, hotels, restaurants and coffee shops) as well as door to door commerce.

2. Environmental and socio-economic benefits generated by the CONAI system

The Life Cycle Costing (LCC) method was created and finalised in 2015, with the support of Studio Fieschi, that also collaborates with the European Union in the field of life cycle evaluations.

Environmental and economic benefits generated thanks to packaging recycled by consortiums and independent management, are monitored through a dedicated tool that is updated on a yearly basis. The method and the Tool have been shared with the six consortiums in order to create an evaluation model that is founded on the Life Cycle approach, which starts from the availability of single fractions and ends with recovered material, electricity and thermal energy produced through energy recovery (attributional approach). The environmental effects were also modelled and computed according to a system expansion (consequential approach): evaluations according to a consequential approach allow to quantify the effects of circular economy adopted by the CONAI system – consortium system in terms of direct and indirect environmental and economic benefits, i.e. environmental external effects.

This model generates three categories that indicate performances:

Energy and matter recovery:

- matter recovered from recycling;

- electricity produced from energy recovery;

- thermal energy produced from energy recovery.

Environmental benefits:

- primary material saved thanks to recycling;

- primary energy saved from CO2 recycling;

- prevented CO2 production from recycling;

- prevented CO2 production from energy recovery.

Life Cycle Costing;

- direct system costs;

- direct benefits: economic value of matter recovered through recycling; economic value of electricity and thermal energy produced from energy recovery; economic activities generated by the system;

- indirect benefits: economic value of CO2 emissions avoided through recycling and energy recovery.

These indicators were calculated between 2005 and 2017, from primary data gathered used to report on single packaging flows, validated in the field of the “Obiettivo Riciclo” (Objective: Recycling) project, a project created by CONAI, aimed at validating procedures used for all packaging material flows in order to determine the data on products released for consumption, recycling and recovery, through a third party specialized body. The validation of procedures that determine the results of recycling and recovery perform a vital role in the field of refining and improving the quality of data made available by CONAI – in accordance with its role, which is to guarantee the achievement of overall recycling and recovery objectives for every single industry – and is one of the main objectives.

When reading the data, we must consider that the model records variations in conferred and recycled material, as well as any possible change determined by secondary data updates. This aspect must not be underestimated from a methodological point of view, since some factors influence the model’s data, for example: the impact of the evolution of technologies employed in various sectors, especially regarding emissions from primary unit material saved. In this case, the best available data are applied in order to represent the technologies and processes, and it is plausible that the benefits of recycling will diminish as industrial processes become more efficient and technologies evolve. Nevertheless, since the data are updated with predetermined expiry dates, changes are recorded non-linearly according to how often European databases are updated.

2.1 Raw material savings

The use of a secondary raw material obtained through recycling in production allows to save a good amount of raw material.

Methodologically speaking, in order to evaluate the benefits of product (packaging) substitution, primary material saved was calculated for each industry, i.e. the amount of matter created with raw material within the packaging itself: substitution factors enable the evaluation of the raw material quota that was not produced thanks to the use material obtained through recycling.

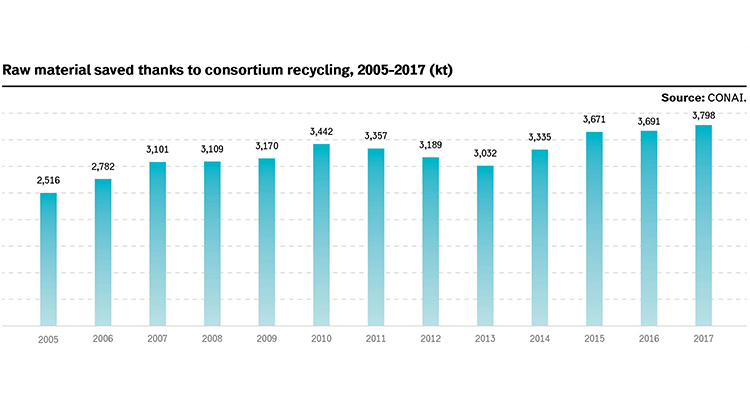

Packaging recycling in 2017 avoided the consumption of approximately 3.8 million tons of raw material: nearly 50% more compared to 2005. 38% of these raw material savings can be attributed to the secondary raw material produced by glass packaging recycling: approximately 1.4 million tons, the equivalent of four billion 0.75 litre glass bottles; 23% of saved raw material comes from the collection and recycling of paper and cardboard: 870,000 tons, the equivalent of 870,000 A4 paper reams. The numbers for recycled wood are very similar: 848,000 tons, the equivalent of 39 million pallets; 400,000 tons of natural resources were saved thanks to the recycling of plastic, the equivalent of 9 billion detergent flacons (1 litre PET containers). Packaging waste recycled through consortium management has also saved 240,000 tons of steel, the equivalent of the weight of 625 Frecciarossa ETR1000 trains, and 13,000 tons of aluminium, or approximately one billion 33 cl cans.

The trends for saved raw material recorded between 2005 and 2017 shows a mostly linear and positive development, with a 25% improvement in 2017 and reaching the historical maximum. On the whole, Italy has avoided the consumption of more than 42 million tons of raw material between 2005 and 2017.

2.2 Primary energy savings and energy recovery

Recycling allows to save large amounts of energy and therefore, CO2 emissions, the main greenhouse gas responsible for climate change.

The primary energy saved through recycling is the amount of primary energy from fossil fuels substituted by energy recovered on the market, calculated according to the amount of energy consumed for the production of raw material from fossil fuels and the amount of raw material saved by recycling single fractions.

Overall energy savings from recycling carried out by the CONAI system in 2017 were equal to 19,4 billion TWh of primary energy, +72% compared to 2005. The total amount of energy saved between 2005 and 2017 amounts to 203 billion TWh, the equivalent of the energy used by 117 thermoelectric plants; 35% derives from the recycling of plastic packaging carried out by Corepla, 27% from the recycling of glass packaging carried out by CoReVe, 24% from paper recycling by Comieco, 10% by steel recycling managed by Ricrea, 3% by wood and 1% by aluminium, respectively managed by Rilegno and CiAl.

Trends have been positive and constantly growing through the years, even when the economy slowed down and the amounts of packaging material used in recycling decreased.

We must also consider the electricity and thermal energy used for the packaging waste that cannot be recycled and is therefore used for energy recovery.

Electricity produced through energy recovery is calculated according to the amount of conferred material that is used for energy recovery and the amount of electricity produced by energy recovery for material units, per single fractions.

Thermal energy produced through energy recovery is calculated according to the amount of material used for energy recovery and the thermal energy produced by energy recovery for material units, per single fraction.

The production of thermal energy and electricity mainly derives from plastic packaging waste, that generated approximately 0.13 TWh of electricity and 0.26 TWh of thermal energy in 2017. The total amount of electricity and thermal energy produced by packaging wasted used for energy recovery between 2005 and 2017 was equal to 5,7 TWh.

2.3 Avoided greenhouse gas emissions

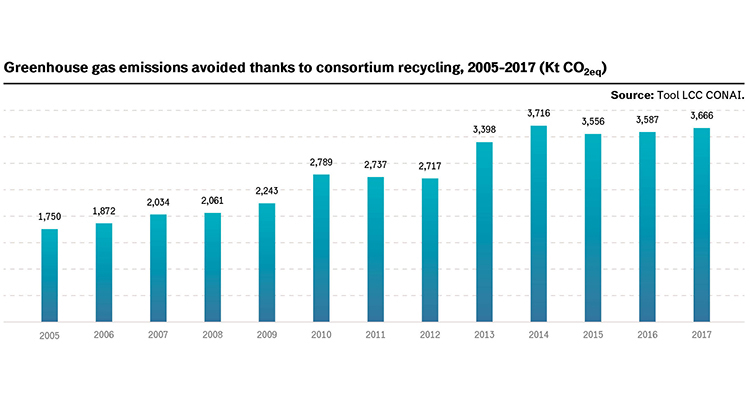

Recycling activities carried out by consortiums in 2017 have avoided the emission of approximately 3.7 million tons of CO2eq in 2017, this number is two times greater than the one recorded in 2005. The total amount avoided between 2005 and 2017 is more than 36 million tons of CO2eq, the equivalent of the emissions of 11 million vehicles with an average travelled distance of 20,000 kilometres in the course of one year. Recycled glass packaging contributed to 34% of this number, paper to 33%, plastic packaging 7%, steel packaging 12%, whilst wood and aluminium respectively contributed to 3% and 1%.

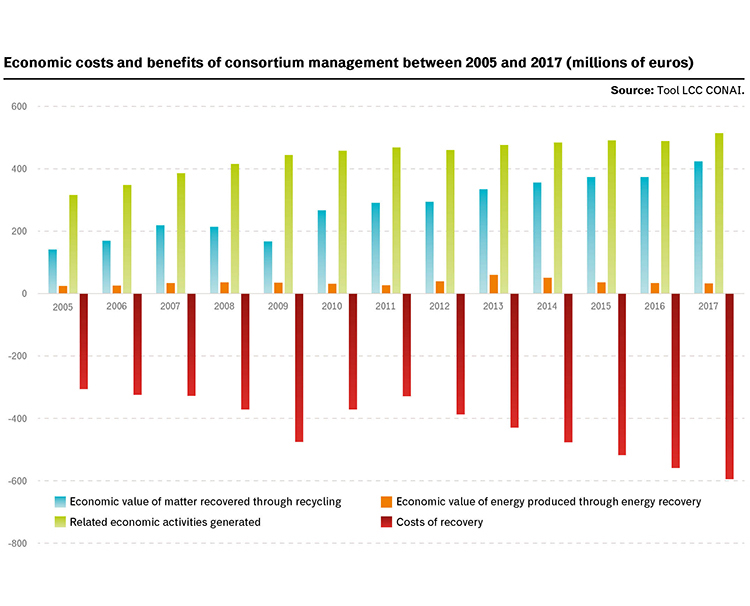

2.4 Costs and benefits of consortium management

Economic benefits correspond to the environmental benefits generated by the recovery of packaging; these were measured using the Life Cycle Costing Tool.

We must underline the fact that the numbers cannot be directly summed in order to reproduce a total net balance (since the reference boundaries do not coincide). Nevertheless, the overall number is shown in order to demonstrate the importance of the economic contribution provided by CONAI and the six Consortium industries to the whole country-system.

Economic benefits connected to the activities carried out by consortiums are both direct and indirect. The direct benefits generated by the consortium recovery industry were equal to 970 million euros in 2017: two times more than 2005. On the whole, it is possible to estimate that the consortium packaging waste recovery industry has generated of 9.8 billion euros of economic benefits for the whole country between 2005 and 2017.

Direct benefits fall under three main categories.

1) Economic value of secondary raw material produced through recycling; calculated according to the economic value of each recovered matter unit and the amount of matter recovered by recycling every single fraction. The economic value of raw material produced through recycling in 2017 was equal to 424 million euros, a number three times higher than the one recorded in 2005. On the whole, we estimate that secondary raw material from recycling generated approximately 3.6 billion euros.

2) Economic value of energy produced through energy recovery: calculated according to the economic value of the units of electricity and thermal energy produced and the quantity of electricity and thermal energy produced per single fraction. The economic value of energy produced in 2017 was equal to 32 million euros (+33% compared to 2005). The total amount of estimated economic value between 2005 and 2017 is 460 million euros of energy produced from energy recovery.

3) Related economic activities: an estimate carried out according to the number of employees that collect and prepare materials for recycling, as well as their salary. The economic benefits generated by related economic activities between 2005 and 2017 was estimated to be approximately 5.7 billion euros.

Indirect benefits are represented by the economic value of avoided CO2 emissions; in 2017 they were equal to 105 million euros, more than twice the number for 2005. It is possible to estimate that these benefits amount to one billion euros between 2005 and 2017.

Estimated direct costs of consortium management were 596 million euros in 2017, and are divided as such:

- 507 million euros for conferral and withdrawal, made up of “conferral and withdrawal costs from public areas” (ANCI-CONAI conferral) and the “conferral and withdrawal costs from private areas”;

- 13 million euros used for exploitation, calculated according to the cost of recycling, energy recovery and other forms of disposal and incomes from sold materials;

- 76 million euros of operating costs for the CONAI system – consortiums (CONAI Balance).