Corepla’s contribution to the implementation of circular economy is articulated in various sectors. The Consortium operates according to the principles of sustainability and its three dimensions: environmental, social and economic. The collection of plastic packaging in 2017 has surpassed one million tons thanks to the collaboration between local administration and the consortium, growing especially in southern Italy and showing an increased per capita collection rate. Municipalities and/or consortium members receive an economic compensation in correspondence to the amount of conferred material and based on the presence of “extraneous fractions” in plastic packaging per ton, according to what was established by the ANCI-CONAI agreement. In 2017, the consortium obtained 310 million euros, more than 55% of its balance.

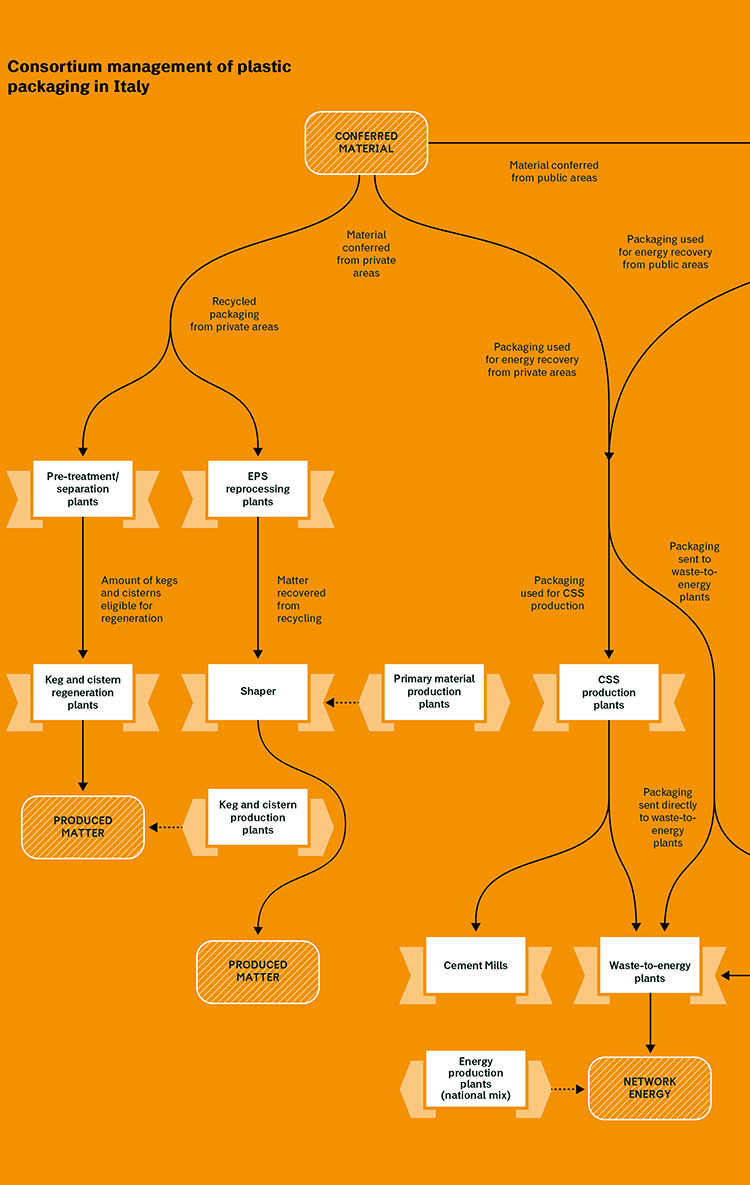

The material is given to selection centres that divide the incoming mixed packages in homogeneous flows for Corepla; this material is then recycled, but one of the flows is destined to energy recovery. Selection centres receive an economic income from Corepla for every ton of material they process. Even though Corepla is bound by the mix of packaging present in separate collection, it carries out an active role in supporting the recycling industry, orienting the selection process (carried out by automated machinery) towards the needs of recycling companies. To this day, the Consortium selects 14 different packaging flows destined to recycling, more than most European countries, that often separate only the types of packaging that can be easily recycled. Corepla has decided to give recycling material only to certified European recycling companies, no material is given to waste traders. This choice ensures transparency, competitiveness and the presence of resources on the European territory, following the logic of circular economy.

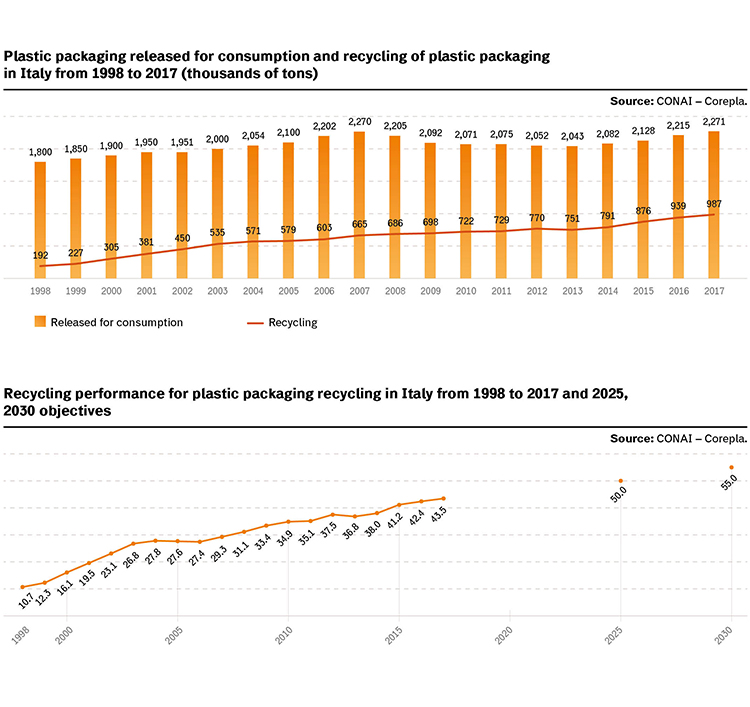

Even though the increase of waste collection has also increased the amount of packaging that is more complicated to recycle, the amount of packaging recycled by Corepla have increased by 6.7% in 2017. The Consortium’s objective for 2018 is to improve on these results, increasing the amount of collected and recycled packaging, in order to give a solid contribution towards the achievement of the recycling objectives set by the recently instated European norm. Knowing that the amount of recycled plastic packaging on a national level in 2017 was 43%, the rate of recycling must increase by 1% every year in order to reach the 2025 objective (55%). This is a particularly challenging objective, and in order to achieve it the Consortium decided to invest in Research & Development, a sector that covers a catalysing role in new projects that involve the whole plastic packaging industry and promotes new packaging solutions as well as new selection and recycling technologies, in order to optimise the balance between market and end-of-life necessities.

It is necessary to create an industry where Corepla is just one of many actors of the packaging recycling process, and it should follow some basic principles:

- companies that use packaging must consider recyclability as one of the main requisites when designing and selecting the types of packaging that will be used;

- Municipalities and citizens must carry out separate waste collection;

- Corepla must carry out the selection of recyclable packaging in homogenous flows, that can be connected directly to the machinery used in recycling companies;

- recycling companies must convert waste into raw and secondary materials;

- processing companies must use raw and secondary material to create new products.

Every part of the industry must be able to operate in a sustainable manner (environmental, technical and economic). If some materials, like PET bottles for water and beverages, are already solidified within this industry, other materials present some technical and economic obstacles that hinder production or functioning and cause some types of packaging to be impossible to recycle.

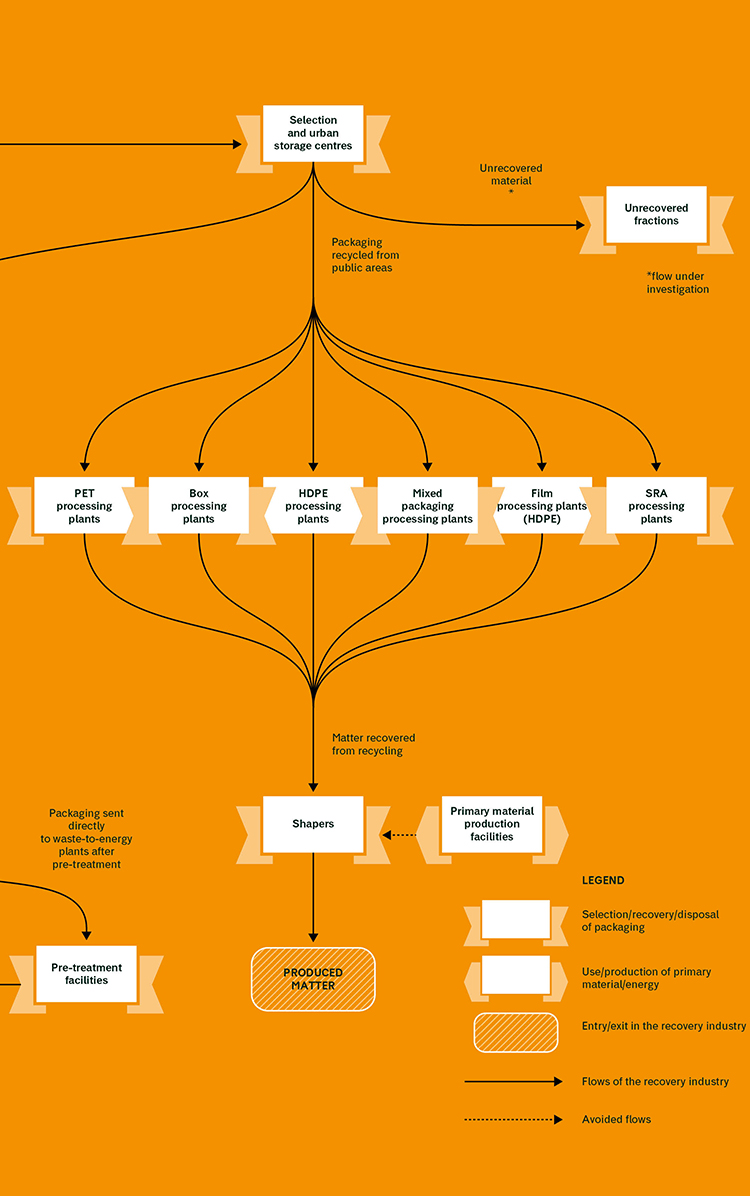

Selected material flows are subdivided into three macro-categories.

- Easily recyclable materials (PET bottles, HDPE flacons and large films). These materials already belong within consolidated recycling chains. Their selection is based on standardised characteristics and this type of plastic is sold to recycling companies through a telematic auction, that can be attended by certified European recyclers. Telematic auctions have been recently extended to part of rigid polyolefin and polypropylene packaging flows.

- Low recyclability materials (rigid and flexible polyolefin, small films) and experimental selected materials. These materials have been attributed a very low or null value and come from experimental or partially consolidated recycling industries, therefore, their quality cannot be standardised. They are given to interested recycling companies, mostly through commercial negotiations. In this case, the recycling company must also be certified.

Corepla’s objective is to recycle an increasing amount of plastic packaging, that in some cases must be selected and modelled according to the needs of the recycling company, or in the case of materials that are harder to recycle, the material is given with an economic contribution towards recycling. Furthermore, continuous experimentations to improve quality of selected materials are taking place, aimed at increasing the percentage of recycling compared to energy recovery, and with the mid-long term objective of creating solidified recycling chains that allow a standardised selection on the national territory and a shift to sales through telematic auctions. - Residual material flow, primarily used for energy recovery, is made up of packaging that cannot be recycled for economic or technical reasons. This situation may be caused by various factors, for example, the size and shape of a specific type of packaging may hinder its selection or recycling, quantities may be too low to justify the creation of a homogenous flow or the lack of interest from the industry, since recycling companies have no contact with markets where the raw and secondary materials produced from this specific type of packaging may be introduced. A large part of these materials is used for energy recovery in waste-to-energy plants or in cement plants, and a minimal part is used as a reducing agent in steel mills instead of coal.

The recycling chain can be improved upstream by creating recyclable packaging (design for recycling) and downstream, by stimulating the demand for recyclable plastic material, for example through the Green Public Procurement instrument and the voluntary choice of large businesses to to use a percentage of recycled plastic in their products in order to make them more environmentally sustainable. The choice between virgin or recycled plastics made by processing companies is mostly based on economics.

The whole system operates on the principle of the producer’s extended responsibility, according to which the producer or imported of plastic packaging bears the costs in order to reach the recycling objectives set by the legislator. This takes place through the CAC (CONAI Environmental Contribution). Both CONAI and Corepla are non profit organisations, therefore these contributions go towards covering the system’s deficits. Sales revenues from materials selected by recycling companies are insufficient, therefore the system could not work without the CAC. Corepla operates according to efficiency criteria, showed by the continued reduction of fixed cost for every ton of managed waste collection, that dropped from 19 euros/ton in 2013 to 13.40 euros/ton in the current year.

On the 1st of January 2018, the CAC instated a new diversification policy for plastic packaging. This is the last step of a long journey that started in 2015, involving the whole industry through continuous dialogue with producers and packaging users. The CAC per ton of released plastic packaging is no longer fixed, it is now modelled on the basis of three Guiding Criteria: selectability, recyclability and for packaging that satisfies these two criteria, the prevalent destination circuit. Three contribution brackets have been created (A, B and C). Recyclable and selectable packaging from “domestic” circuits has been facilitated (bracket B) and even greater advantages were given to packaging coming from the “Commerce & Industry” circuit (Bracket A); all other types of packaging continue to pay the full contribution (bracket C). Since the system operates from a non-profit perspective, the lower income coming from the lower contributions of brackets A and B are compensated by the higher income from bracket C. The brackets assigned to various types of packaging are not definitive, selectability and recyclability may change in time and according to the types of packaging released into the market and the evolution of selection and recycling processes.

A periodic revision mechanism will soon be activated. The objective of contributory diversification is to reward the companies that create selectable and recyclable packaging as well as stimulating the companies that use bracket C packaging to start projects aimed at improving their selectability and recyclability. A series of guidelines have been drawn up in order to aid companies that produce and use packaging publicised under the CONAI umbrella.

Environmental and socio-economic benefitsof consortium management

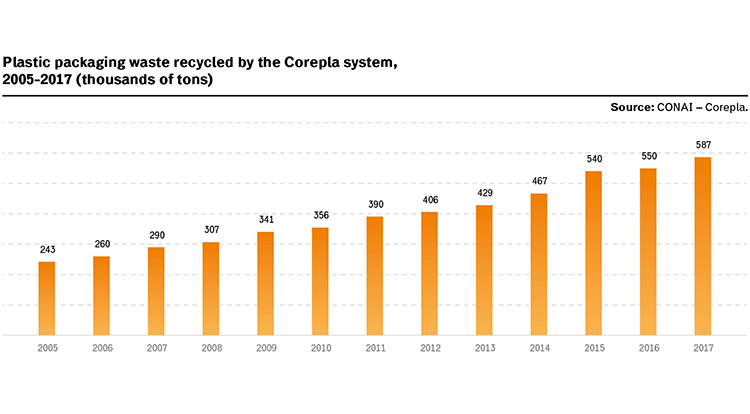

The Consortium recycled 587,000 tons of plastic waste in 2017, approximately 59% of the total plastic recycled in Italy during that year, including independent management. This result was reached after a period of progressive and sustained growth, that saw the material recycled by Corepla double in size compared to 2005 (the first year for the CONAI LLC Tool).

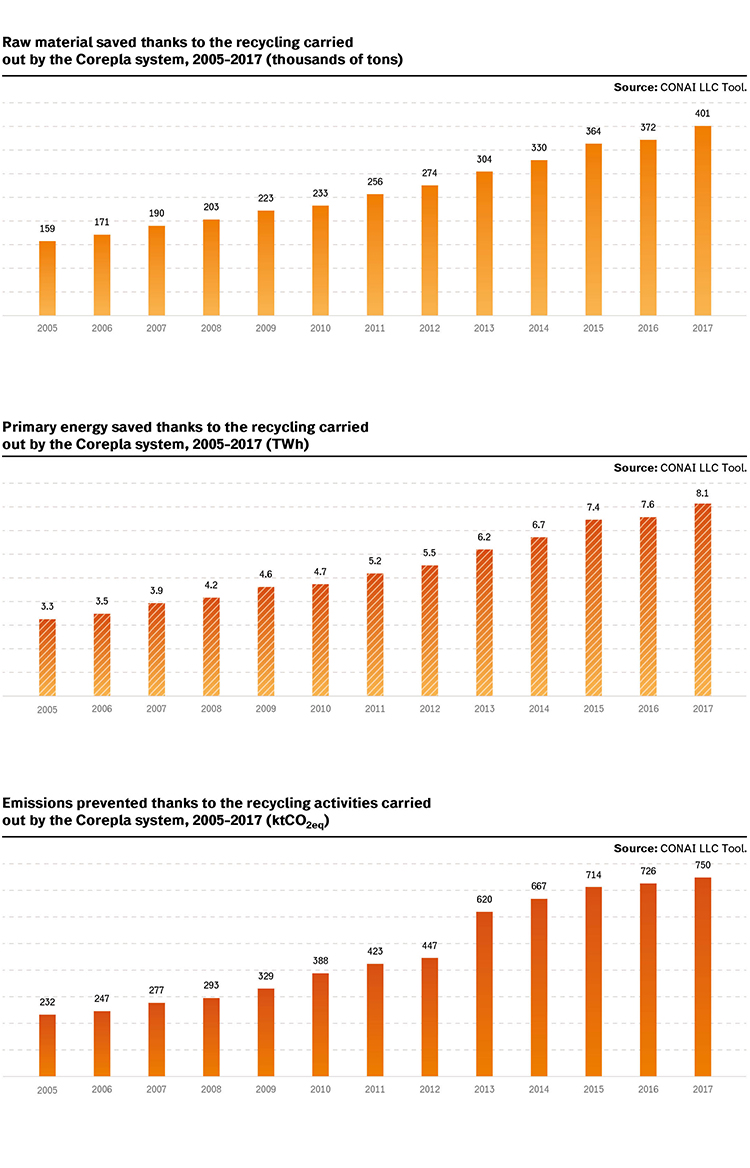

According to the results of the LLC Tool developed by CONAI, the recycling activity connected to plastic packaging waste coming from separate waste collection in public and private areas carried out by Corepla prevented the use of more than 3 million tons of raw material between 2005 and 2017, the equivalent of 78 billion PET 1 litre detergent flacons.

The trend of raw material saved thanks to recycling has shown a constantly growing development in the last 13 years: the amount of raw material in saved in 2017 is two times what was saved in 2005, due to the fact that the quantity of recycled material shows a gradual increase in the course of the years, showing marked growth rates for PET and mixed plastic packaging.

The recycling carried out by the Corepla consortium prevented the use of 401,000 tons of raw material (material generated from fossil fuels) in 2017, 2% more than 2016, due to an increase in conferred and recycled material (+6.7% compared to 2016).

On the whole, the Consortium’s recycling activity has allowed Italy to save approximately 71 TWh of primary energy between 2005 and 2017, the equivalent of the primary energy used by 42 thermoelectric power plants. Trends for primary energy saved through the years show a steady development, in accordance with the data concerning material recovered through recycling that we displayed previously, showing a twofold increase between 2005 and 2017; this increase can be mainly attributed to the growth of the PET and mixed packaging quota.

The energy saved in 2017 thanks to the recycling of plastic packaging managed by Corepla was equal to 8.1 TWh of equivalent primary energy, 7% more than 2016.

The emission of 6 million tons of CO2eq was avoided between 2005 and 2017, mostly due to lower energy consumption deriving from the use of recovered material; these emissions are equal to those produced by 2 million vehicles with an average travelled distance of 20,000 kilometres in the course of one year. The emission avoided thanks to recycling also show a constantly increasing trend in the course of the years, and have more than tripled between 2005 and 2017.

The recycling of plastic packaging carried out by the Consortium in 2017 prevented the emission of 750,000 tons of CO2eq, 3% more than 2016.

We must also consider the benefits of electric and thermal energy produced through the energy recovery of unrecyclable plastic packaging waste. The amount of electricity and thermal energy produced from energy recovery both show an uneven trend, caused by the variation in the relationship between the amount of material destined to waste-to-energy plants and the material sent to cement factories (part of the packaging sent to waste to energy plants was shifted towards cement factories). On the whole, the energy generated by energy recovery in the course of 13 years was 5.5 TWh, the equivalent of the primary energy used by 3 thermoelectric power plants, 33% represented by electricity and 67% by thermal energy. The energy generated between 2005 and 2017 has increased by 35% (the GWP index is computed as a net balance between prevented emissions and emission produced for recycling preparations). The use of non recyclable material for energy recovery carried out by Corepla generated 0.4 TWh of electricity and thermal energy in 2017. We must also point out that in addition to saving primary energy, the production of thermal energy and electricity from non recyclable waste gives way to a process that has generated 199,000 tons of CO2eq in 2017.

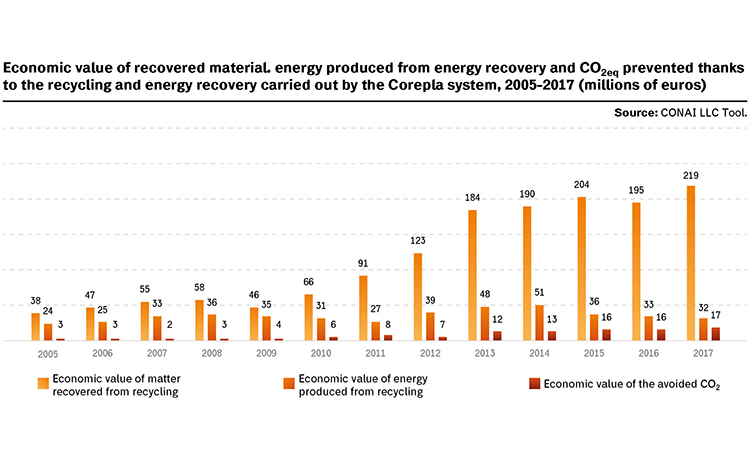

We can deduce a series of direct and indirect benefits for the country-system from the environmental benefits we listed above. It is estimated that the consortium plastic packaging waste recovery industry has generated an economic value of 236 million euro 2017 (quadrupled from 2005). The accumulation of these benefits from 2005 to 2017 has reached a total of 2 billion euro divided into:

- 1.5 billion euros of direct benefits generated by the consortium plastic packaging recycling industry, represented by the economic value of saved raw material; these benefits were equal to 219 million euros in 2017 (more than five times the amount for 2005);

- 110 million euros of indirect benefits referring to the amount CO2eq avoided thanks to the recycling and energy recovery activities carried out by consortium management; the total for 2017 is 17 million euros (five times the estimated value for 2005);

- 450 million euros of direct benefits referring to the energy produced through energy recovery; the total for 2017 was 32 million euros (+33% compared to 2005).

Top image – Credit: Corepla/graphic elaboration